Why high-value Shopify merchants lose sales at checkout and what to do about it

This one goes out to all the furniture stores, jewelry brands, and made-to-order brands selling products that cost several hundred dollars or more, where every abandoned cart stings.

When your checkout aligns what customers pay with what they're actually getting, the right customers move forward with more confidence.

Cart abandonment advice wasn't written for you

If you're selling high-value products on Shopify, your abandoned cart rate probably looks worse than most. Over all of 2025, the average was close to 80% in industries like furniture, jewelry, and fashion.

The standard advice? Send a recovery email, add urgency, or throw in a discount.

But that wasn't written for you. It was written for the merchant selling $40 candles.

When someone walks away from a made-to-order dining table set or a custom engagement ring, something different is happening.

It's hard to recover from looking at your abandoned carts!

The math of their hesitation is different. The emotional weight of that commitment is different. And the solutions need to be different, too.

This article breaks down the three real reasons high-value shoppers abandon and what you can actually do about each one.

Not all abandoned carts are worth chasing

Before diving in, it's worth saying plainly: some abandoned carts aren't worth chasing.

A chunk of shoppers were never going to buy.

They're price-comparing, using your cart as a wishlist, or abandoning on purpose to see if you'll send them a discount code.

For high-AOV stores, this behavior inflates your abandonment numbers without reflecting real purchase intent. Trying to fix it will lead you in circles.

The more useful question: Why are the people who genuinely want your product still leaving?

That's what the rest of this article is about.

Problem 1: Paying the full price upfront feels like too much

Extra costs at checkout, such as unexpected shipping fees, taxes, and other add-ons, are the top reason shoppers abandon carts, cited by 44% of customers. For lower-priced products, that's mostly a transparency problem: show the true cost earlier, and many of those shoppers come back.

For high-value items with lead times, though, the problem runs deeper. It's not just that costs are surprising. It's that the total commitment itself feels like a lot.

Industries with higher-price items like home furnishings and jewelry see significantly higher abandonment rates. Buyers already take a long time to decide on making purchases in this category. Combining that with large upfront costs makes buyers hesitate even more.

Paying $800, $1,600, or $5,000 upfront, before the item exists or ships, is a different kind of ask. Especially right now, when cash flow is tight and economic uncertainty makes every large purchase feel heavier.

One merchant using the Shopify deposit app Downpay described it well: customers aren't nervous about the price. They're nervous about tying up their money for an unknown amount of time. That's a different problem, and it needs a different solution. (There's a big hint in this paragraph.)

What actually helps

The most direct fix is changing what "commitment" looks like at checkout.

Instead of asking for the full amount upfront, you can offer (guess what?) a deposit. Typically high-value merchants charge 30 to 50% at checkout, with the balance collected when the item is ready to ship.

Deposits also create a useful operational benefit beyond conversion: customers who've paid something for preorders, backorders, and made-to-order goods have skin in the game.

The "notify me when it's back in stock" email list is full of people who will get distracted and go elsewhere. A deposit order is a real order.

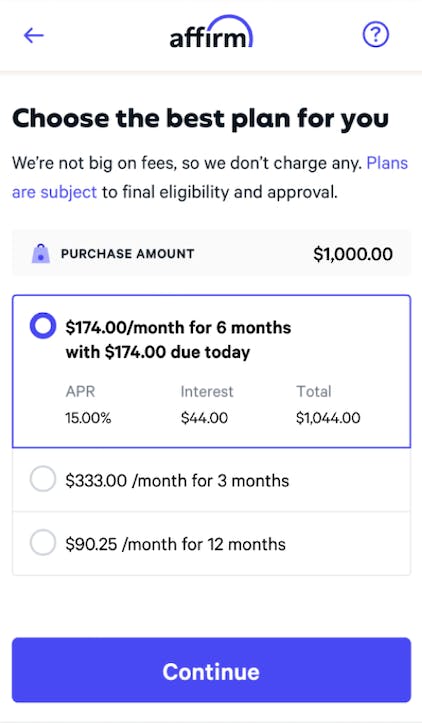

Affirm BNPL plan selection

Why deposits aren't the same as Buy Now, Pay Later

At this point, a common question is "Can't I just offer a BNPL solution like Affirm or Klarna? I get cash upfront and my customers don't have to pay all at once."

We're going to take a quick detour to cover this before moving on to problem #2, since it's relevant to Problem 2 and Problem 3.

BNPL

The truth is, Buy Now, Pay Later is designed for a different type of seller: merchants with low-value items in stock. And for high-value merchants, BNPL often creates new issues.

A quick run-down on BNPL services:

- They're financing products, a new iteration of consumer loans.

- They involve buyer credit checks and approvals.

- They charge high merchant fees that can eat 5 to 10% of your margin on every order.

For a $1,500 item, that's real money leaving your business on every sale. And for very high-value products, BNPL providers will sometimes decline the transaction entirely because the loan amount is too large.

Deposit-based checkout works differently.

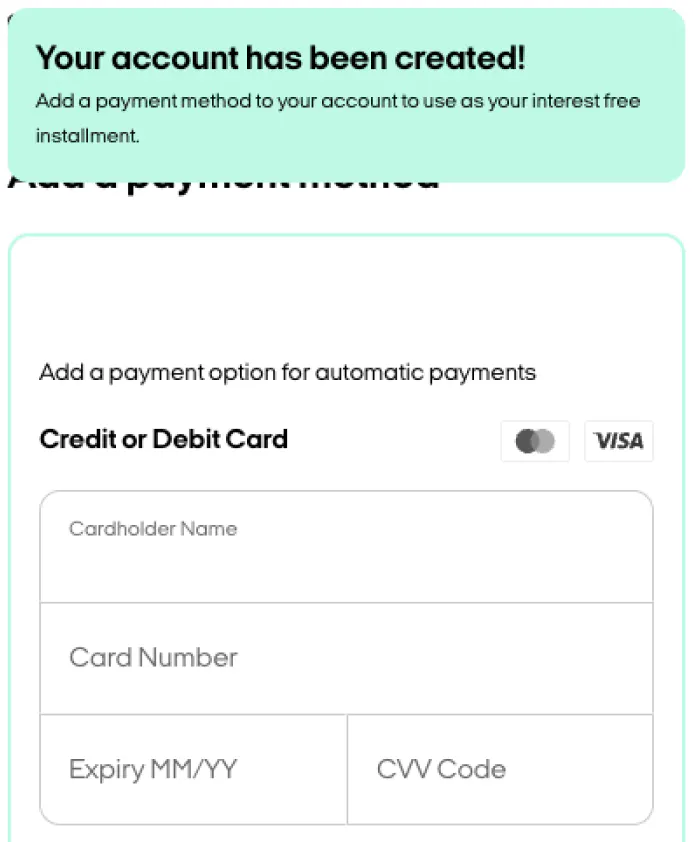

Deposits on Shopify

Using Downpay, the Shopify-native deposit app:

- The customer uses their own card to pay the deposit at checkout. No loans, no credit checks.

- You collect the balance on fulfillment from their card on file, manually or automatically.

- You don't lose margin on every transaction. (Downpay charges a monthly fee, not a transaction fee.)

- The customer gets breathing room they need to say yes. No predefined payment intervals and no unnecessary sales team back-and-forth.

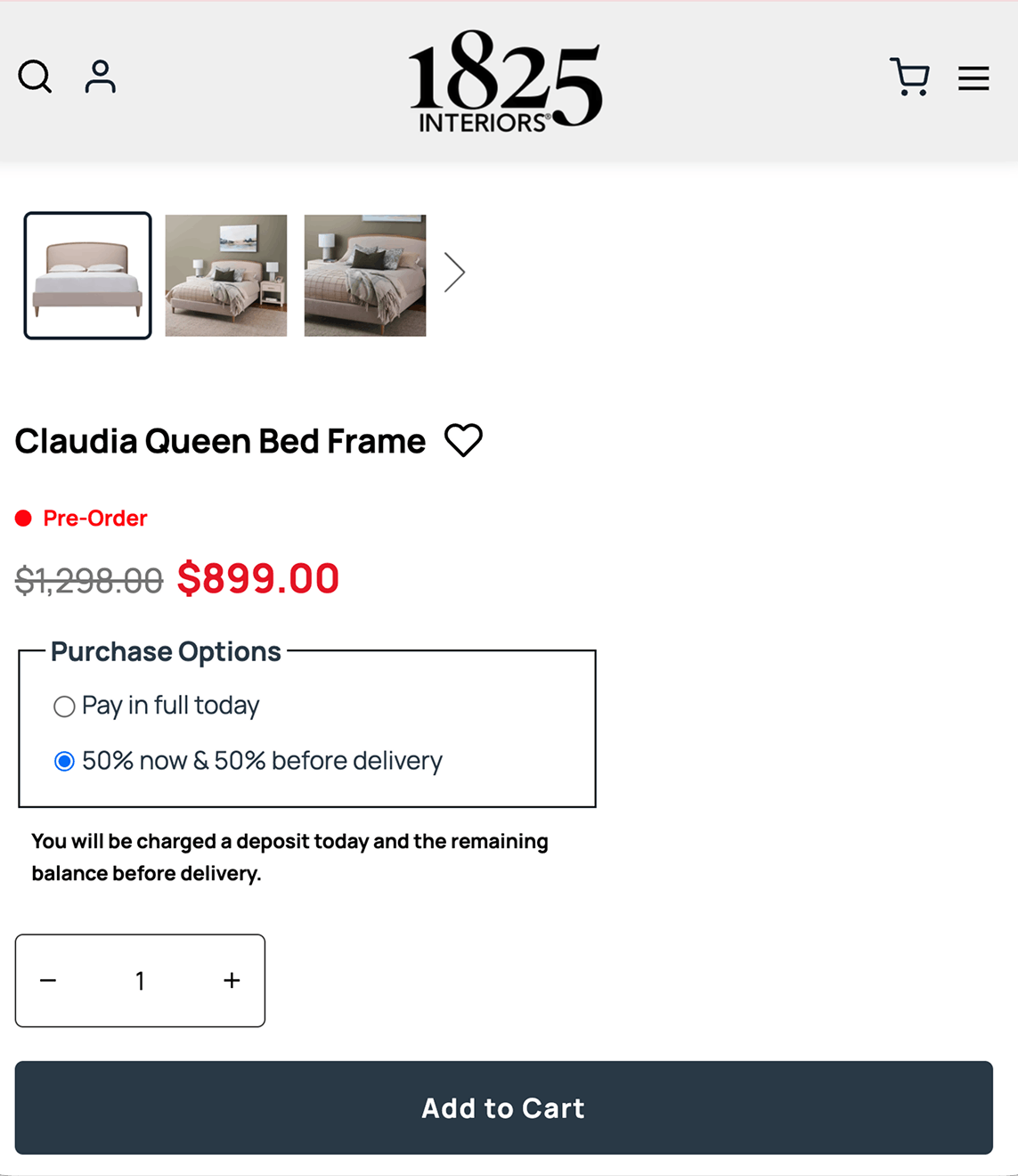

1825 Interiors product page using Downpay to offer a deposit purchase option

This distinction between BNPL and deposits also matters for checkout friction—the next major problem we're going to cover.

BNPL providers advertise a seamless experience, but in practice these apps add difficulty that can deter high-value buyers. More on that below.

Problem 2: Checkout friction is killing your high-value conversions

Long or complex checkouts account for 22% of cart exits, the second most common reason shoppers abandon.

It's easy to see why: on average, these flows have 5 steps and 11 form fields, with every extra step an invitation to reconsider.

And for a $900 purchase, that invitation lands harder than it does for a $30 one.

Other common breaking points—along with the share of shoppers who cite it as a reason for abandoning—include:

- Re-entering credit card info: 30%

- Forced account creation: 26%

- Long or complex checkout: 22%

- Full costs not shown until checkout: 21%

And on mobile, friction compounds fast, explaining why 13% more carts are abandoned on mobile than desktop.

Afterpay Buy Now, Pay Later new account creation.

This is another difference between BNPL and Shopify deposits: Buy Now, Pay Later services advertise a frictionless experience, but in practice they add friction of their own.

Right at the moment of decision, customers can get spooked when they encounter many of those same breaking points:

- An external payment system with its own approvals

- Required account sign-up

- An unfamiliar interface outside of your branded Shopify Checkout

- An opaque fee structure

Solving a price hesitation problem by introducing a checkout complexity and trust problem is not a trade worth making.

What actually helps

- Limit steps wherever possible. Shopify's checkout is already best in class. Adding apps that bolt on new interfaces or redirect to external flows works against you.

- Use solutions native to Shopify. With Downpay, for instance, customers can enter card details once for both payments. Or they can even use saved Shop Pay details and not have to enter it at all. See how deposit checkouts look across industries.

- Audit your checkout on a phone. On mobile, every extra tap matters. If you're cringing, your customers are too.

- Show costs early. Surface estimated shipping on product pages before the customer even reaches the cart. Don't let the total be a surprise at the end.

Problem 3: Pre-order anxiety and why unclear timelines cost you sales

Shoppers often abandon carts because they're unclear on what happens after they place the order.

For products with long lead times or custom production, the uncertainty piles up fast.

Preorders and made-to-order products create a specific version of this problem. If a customer is paying upfront but doesn't know when the item ships, or what happens if there's a delay, they're being asked to make a leap of faith. Some will. Many won't.

This matters especially for high-value products, where the stakes of getting it wrong feel higher to customers.

Someone who paid $1,200 upfront for something that might arrive in six months has a lot of time to regret that decision and a lot of motivation to cancel.

What actually helps

- Show estimated shipping time ranges before checkout, not just at the final step before committing.

- Be explicit about how deposits work. If the balance is collected at fulfillment, say that on the product page, in cart, and at checkout. Don't just bury it in your FAQ.

- Communicate proactively when timelines shift. If your manufacturer is unpredictable, customers would rather know than wonder.

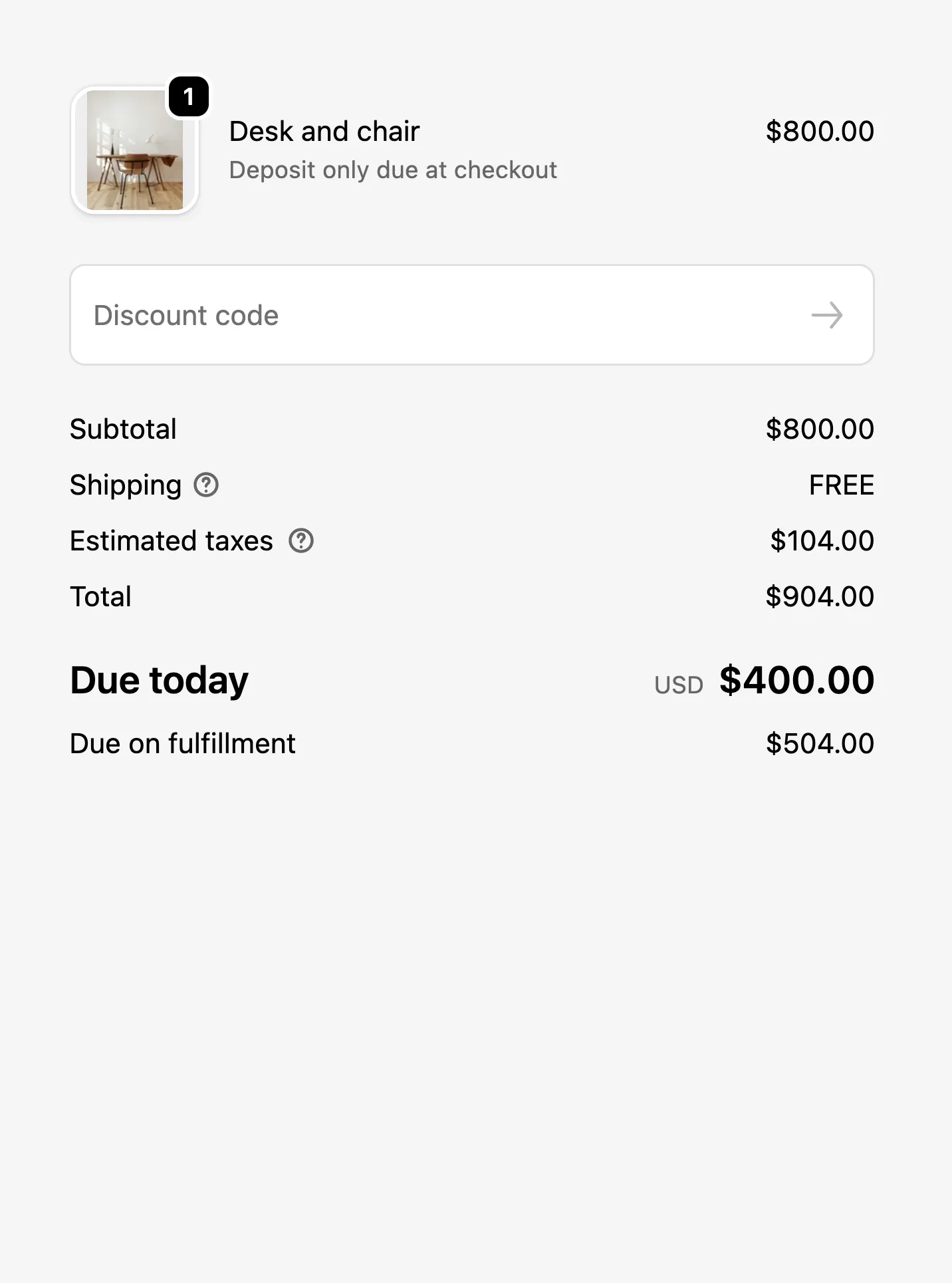

- Make the payment structure visible at every step. "Pay today, rest at fulfillment" is a message that converts, but only if the customer can actually see the subtotals throughout the flow.

Shopify checkout using Downpay for a 50% deposit option on made-to-order furniture.

One practical note: "on fulfillment" as a balance due date is genuinely useful for merchants dealing with unpredictable lead times.

You're not promising a date you can't keep, but you're still giving customers a clear framework for how it works.

Why abandoned cart emails don't fix these problems

Most abandoned cart advice stops at recovery: send an email, add urgency, offer a code.

Recovery can help, and a realistic expectation is a 5–10% recovery rate on those emails.

But an email after the fact doesn't address the reason someone left. The commitment still feels too large. The checkout still had too many steps. The timeline is still unclear.

There's also a perverse incentive problem worth naming: some shoppers abandon specifically to trigger discount codes. Once your customers learn this works, it becomes a habit.

Your abandonment numbers go up, your margins go down, and the metric you're chasing is no longer telling you anything useful.

For high-value merchants specifically, a blanket discount code is a painful solution. Knocking 10% off a $1,500 order to recover a sale that might have converted anyway is an expensive way to feel like you're fixing something.

The more durable fix is upstream: reducing the friction before someone leaves, not chasing them after.

How to collect deposits on Shopify to reduce abandonment

Downpay was built for exactly this kind of store: high-value products, long lead times, customers who want to buy but hesitate at full commitment.

Merchants can collect a deposit at checkout, with the balance captured automatically when the order is ready to fulfill.

The key points:

- Customer cards are stored securely on file by Shopify.

- The flow runs inside native Shopify checkout (so Shop Pay, saved cards, and all existing payment methods still work).

- There's no financing, credit checks, or margin sharing involved.

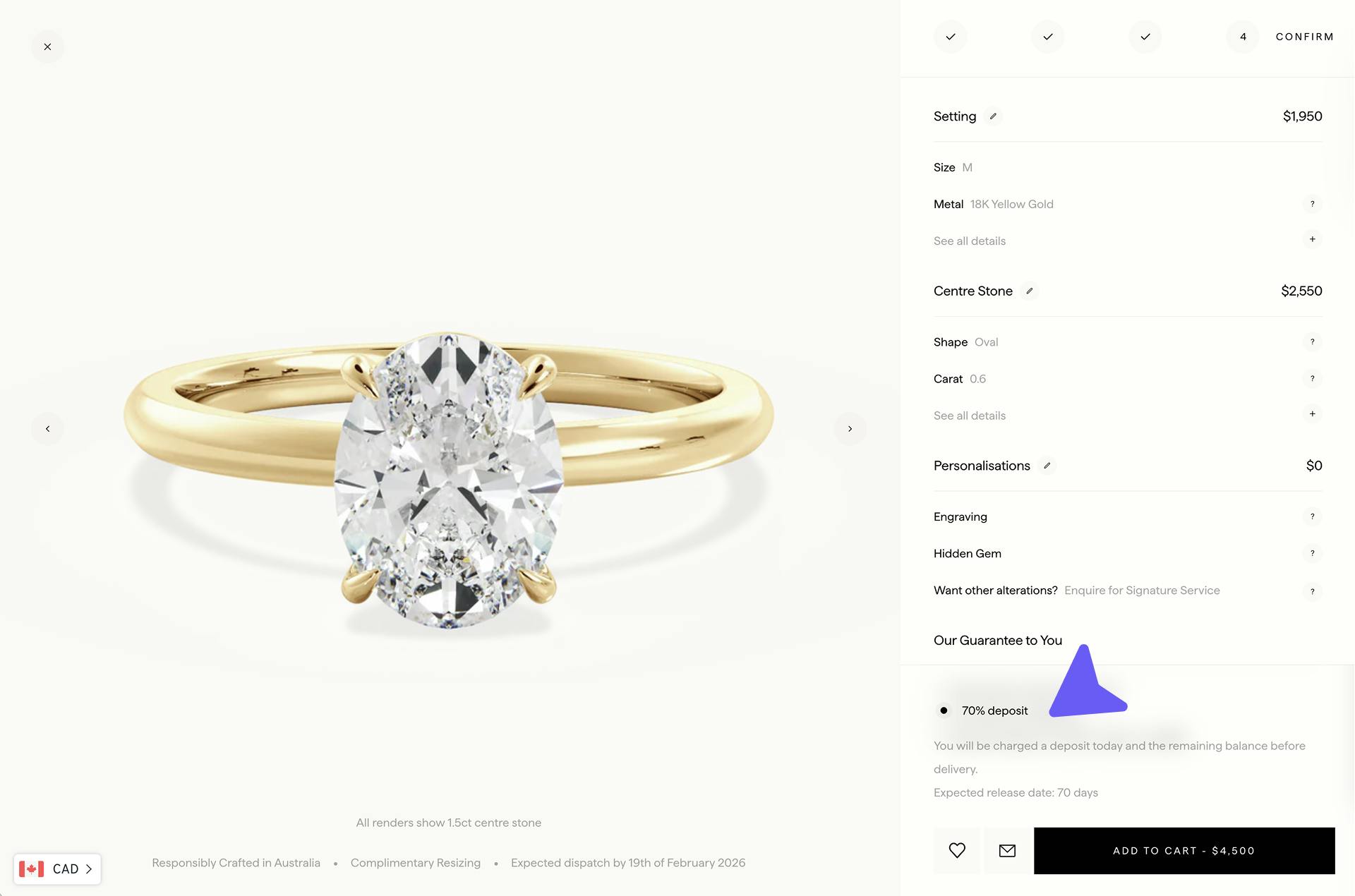

Louise Jean sells bespoke engagement rings, wedding bands and fine jewelry, handcrafted and made to order on Shopify using Downpay.

Where it has the clearest impact:

- Conversion on pre-orders and made-to-order products. Brands typically see 15 to 25% improvement in AOV and meaningful gains in conversion, particularly for products over $800 where hesitation is highest.

- Fewer cancellations. Customers who've committed a deposit are meaningfully less likely to cancel or go silent. If someone can't follow through, you can cancel the order, keep a non-refundable portion of the deposit, and sell to the next person in line, without the communication nightmare that comes from holding full payment.

- Cleaner operations around fulfillment. Balance collection can be automated through Shopify Flow, including reminders, invoices on failed charges, and notifications when payment succeeds. If your timelines are unpredictable, you can bulk-process balance charges when items arrive rather than chasing individual customers.

Downpay doesn't replace your existing payment methods. BNPL, traditional bank financing, whatever you're using for financing can all coexist.

Deposits fill the gap for customers who don't want a loan, just a little breathing room.

Stop optimizing for abandonment rate and start optimizing for order quality

For high-value merchants, the goal isn't eliminating abandonment. It's improving the quality of the orders you do get.

A 3% conversion rate with low cancellations, reliable payment collection, and customers who followed through is better than a 4% rate where 1 in 5 orders fall apart before fulfillment.

When your checkout aligns what customers pay with what they're actually getting, and when the commitment feels proportionate to where they are in the decision, the right customers move forward with more confidence.

That progress might not show up as a dramatic drop in your abandonment percentage. But it shows up in revenue and in trust.

About Downpay

If you want to try out deposits on your store, Downpay is built by Shopify alumni for Shopify merchants selling high-value products. You can explore how it works or try it on a subset of products where abandonment is costing you the most.