The full story on Buy Now, Pay Later for e-commerce businesses

Buy Now, Pay Later (BNPL) apps promise more sales, but drawbacks from high transaction fees to reputation issues can offset the benefits. This guide digs in.

Business risks of offering Buy Now, Pay Later to your customers

Article update

This article was updated March 14, 2025, to reflect the current regulation situation in the United States.

Ever wonder why Buy Now, Pay Later (BNPL) apps all advertise that customers can pay in four interest-free installments? Not five, or seven, or any other number?

Affirm, Afterpay, Klarna, PayPal, Sezzle, Zip—they all work that way, although some now offer more traditional loans with interest as well.

Marshall Lux, Harvard Research Fellow and former Global Chief Risk Officer at Chase Bank, has the answer:

Video from CNBC.

The Truth in Lending Act (TILA) was created in the United States to protect consumers from manipulation by predatory lenders. It covered loans with a certain number of installments. That number? Five or more.

As Lux says:

Coincidence? I don’t think so.

Like any set of laws, TILA isn’t perfect. Regardless, designing a loan product specifically to avoid consumer protection laws doesn’t look great. And no matter the intention, the result is clear: it isn’t great.

Business studies researchers, financial publications, public broadcasters, consumer protection organizations, central banks, and regulators all agree on the central concern. It can be summarized in one bullet:

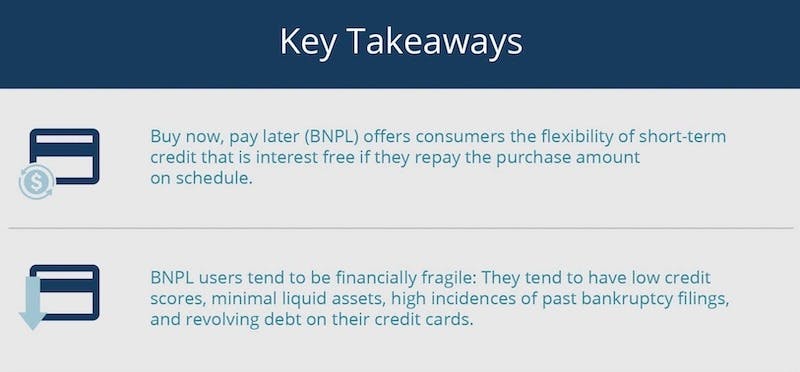

- BNPL apps encourage people who can’t afford it to spend money they don’t have.

A recent report published by the Boston Federal Reserve Bank illustrates both the consumer appeal and the potential harm:

Image from the Boston Federal Reserve Bank.

Because of the identified dangers to customers, this largely unregulated industry is now facing increased oversight worldwide. This still includes the United States, for reasons that will be discussed.

The hazards of using BNPL apps aren’t limited to vulnerable consumers either.

Merchants must also examine the claimed benefits of BNPL and understand the potential pitfalls. The effect of providers’ harmful business practices on your own reputation is just one of them.

Read this comprehensive guide to learn more—in four installments that are hopefully not interest-free:

- How BNPL apps work

- Merchant benefits of BNPL

- Merchant risks of BNPL

- Takeaways for merchants

There’s also a bonus closing statement:

- Bringing back layaway with Downpay

About Downpay

Downpay is an app for collecting deposits on Shopify using a card on file, built by Shopify alumni. An overview of scenarios where Downpay helps merchants secure revenue for high-value items that aren’t yet ready to ship appears at the end of this article.

How Buy Now, Pay Later apps work

BNPL apps have massively increased in usage since they launched in the 2010s. Providers now offer more traditional loans as well as pay-in-four interest-free ones.

US shoppers used BNPL apps for a staggering $1 billion of the total $13 billion they spent on Cyber Monday 2024.

But Jeremy Solomon, former Chief Capital Officer of a BNPL provider, explains how they aren’t a new development:

BNPL is nothing more than a rebranding of purchase finance.

So what’s underneath the slick new paint job?

The history

Purchase finance is a business model that enables customers to make purchases right away while paying for them over time. Also known as consumer financing, it has a long history—and not a spotless one.

Eighty years ago, retailers promised customers a high-tech radio right away in exchange for several easy payments:

Image by Joe Haupt from Flickr.

If the phrase “easy payments” makes you, well, uneasy, that’s with good reason.

Jeremy Solomon, BNPL C-suite alum, explains why:

Purchase finance has a long history of being predatory toward consumers, loaded with hidden fees or deferred interest.

The term “predatory lending” describes lending practices that exploit borrowers. Often, it involves manipulating uninformed or desperate people. They are pushed into taking out loans with unfair or abusive terms. Many consider payday loans a prime example of this.

Debt.org lists several types of predatory practices, including:

- Inadequate or false disclosure: Not disclosing terms, misrepresenting terms, or changing the terms after signing. (Adjusting the terms is what Cory Doctorow calls Darth Vader MBA behavior: “I am altering the deal. Pray I don’t alter it any further.”)

- Inflated fees and charges: Extra charges that are higher than industry averages and often disguised in fine print.

- Risk-based pricing: Offering loans with high interest rates to subprime or even deep subprime borrowers who are at a high risk of defaulting

TILA was established in 1968 to curb what Cornell Law School refers to as “exceedingly predatory” lending.

Image by Andrew Bain from Flickr.

So this is the pre-history.

But what do these apps bring to the table?

Buy Now, Pay Later: The next generation

What makes Buy Now, Pay Later apps unique is how little effort it takes to commit to a loan. (The paint job really is slick.)

Buying from an online store using a BNPL app is almost as fast and easy for customers as paying via a credit card. In fact, many customers use their credit cards to pay down BNPL loans—paying for credit with credit.

Here’s how BNPL works for customers:

- The customer adds products to their cart.

- If they haven’t registered with the BNPL provider yet, the customer registers and links their account to their credit card or bank account.

- The customer initiates checkout and selects BNPL as the payment method.

- The BNPL provider assesses creditworthiness in real time and offers payment plan options to the customer.

- The customer agrees to the terms of the payment plan, completing the order.

- The BNPL provider releases the full order price to merchant minus transaction fees. These depend on order value and merchant plan.

- The customer makes installment payments at scheduled intervals until the balance is paid off.

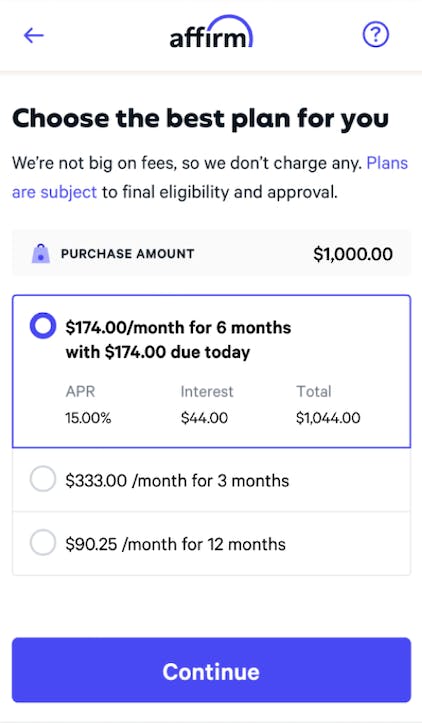

There are two main categories of BNPL loans:

- Interest-free loans (the pay-in-four type discussed at the start)

- Longer-term loans

Interest-free loans

- For purchases below a value defined by the provider in the merchant’s service plan.

- Open to customers who meet the provider’s credit requirements.

- No interest but may charge late fees or other fees.

- Repayment often due in four equal payments, with one every two weeks.

Longer-term loans

- May be the only choice available for high-value purchases or customers who don’t meet credit requirements.'

- Interest rates that get as high as 36% annual percentage rate (APR), depending on purchase value and customer credit.

- Offered through a similar interface as interest-free loans, which can be confusing for customers.

- Repayment usually on a monthly schedule.

Merchant appeal of Buy Now, Pay Later apps

For merchants, BNPL apps build on the attraction of earlier purchase finance models.

Going back to Jeremy Solomon for what that draw is:

Adding a consumer financing tool has consistently proven to increase funnel conversion (more consumers purchasing items) and cart size (consumers spending more) […]

This is the holy grail of commerce.

The main temptations of BNPL apps include:

- Higher conversion and fewer abandoned carts: Hesitant customers may be more likely to complete orders because they can pay in smaller amounts over time and there is minimal friction. The number of potential customers may also be larger as BNPL apps offer credit to people who can’t access it other ways.

- Higher average order value (AOV): Customers may place larger orders because spreading out payments makes them feel comfortable spending more at once.

- Ability to move upmarket: Businesses may drive growth by offering higher value items because customers are willing to spend more.

- Payment up front, minus fees: Merchants can feel comfortable shipping immediately because the BNPL provider takes on the risk of non-repayment.

Another claimed merchant benefit is currently losing its lead over other payment methods:

- Less regulatory burden and expense: Among other shortcuts available due to minimal regulation, merchants did not have to handle chargebacks from US customers using BNPL zero-interest pay-in-four plans, because they were not subject to TILA.

But zero-interest loans from BNPL apps now are subject to regulation under TILA. This happened in spring 2024.

So, guess who’s (charged) back? Is it you? More on that soon.

All that is to say, like in the movies, the true Holy Grail may not be the shiniest one. (Wink, wink.)

Merchant risks of Buy Now, Pay Later apps

In other words, risks to your business can offset all of these potential benefits of BNPL apps. (Maybe not as much drinking from the wrong grail, aging 1000 years and crumbling into dust, but you can decide about that.)

The remainder of this article will cover the following negatives, each including discussion of the claimed positives:

- High merchant fees on high-value items

- More returns of impulse purchases

- Increased regulatory burden as the industry is scrutinized globally

- Service changes affecting key benefits as new companies strive to become or stay profitable

- Reputation impact: Association with harmful practices, entangled processes with poor customer experiences, and increased fraud risk on BNPL transactions

It’ll also cover Downpay, just a little, at the end.

Is it worth it for you? Be your own jury in 2025! Here’s the first risk.

High transaction fees on big-ticket items

In some scenarios, BNPL apps can indeed encourage higher conversion, fewer abandoned carts, and higher average order value.

This does initially suggest businesses could move upmarket by offering higher value goods.

But recent research suggests offering BNPL tends to boost the sales of lower value items more than higher value items.

And for merchants who do see growth in the sales of big-ticket items, the transaction fees could be unworkable.

The higher value the order, the more likely the customer is to default. The incidence of fraud also goes up. BNPL providers then take a larger percentage of each transaction to offset their exposure. This can work out to at least 10%.

Downpay (hi) published a case study focusing on BNPL transaction fees on high-value items. Below is a quick summary.

Case study: Ma Folie

Cathy Shen was looking for a flexible payment solution for her bespoke engagement ring store, Ma Folie.

She first considered setting up a BNPL option, but the transaction fees squeezed her margins too much:

My products are very high value already. So for them to take 8% or 10%, it was just too much for my business to handle.

Image from Ma Folie.

On the sale of a $4000 ring, Ma Folie would be paying $400 to the provider. And in exchange for what?

The customer won’t get the product until they finish payment. So merchants selling custom products or pre-orders don’t need the level of insurance provided by receiving the total up front.

Well, the total minus those sky-high fees.

And higher transaction fees don’t just cost you on sales. They also reduce how much you recover from returns.

More returns

The lack of friction involved in BNPL transactions encourages impulse purchases, which naturally have a higher return rate.

Encouraging hesitant customers to buy has a flip side: a higher proportion of them will change their minds. They may think twice about the cost, or decide that’s not the product or service they want.

Higher average order value and conversion don’t mean as much if those orders are returned and those conversions un-convert.

As the US Chamber of Commerce advises businesses:

Returns are expensive: It costs a company 66% of the price of a product to process a return. In some cases, BNPL could be costing your company money rather than boosting profits.

Image by Russell Lee from Library of Congress.

Transaction fees and returns are relatively straightforward risks. The other issues facing merchants using BNPL apps are more complex, including regulation.

Regulatory issues

Uncertainty in America

As of March 14, 2025, the regulatory situation in the United States is uncertain, to say the least. The US Consumer Financial Protection Bureau (CFPB) may or may not continue to exist, and if it does, its ability to determine compliance with TILA and other relevant laws and enforce them may be limited.

Even without coordinating federal agencies, however, individual states still enforce existing laws. They can also implement their own, which is more likely in the absence of Federal enforcement. In fact, New York already has.

So, don’t discount the possibility that recent changes in regulation will remain and new ones will be created that affect the merchant experience with BNPL apps.

BNPL apps are relatively new, only reaching mass adoption in 2020.

American Express summarized the central concern in 2023:

This is still a new, largely unregulated industry that is finding its footing. There’s no way of predicting what additional hassles or hurdles might present themselves as it matures.

A couple of years later hassles and hurdles have come up. And yes, one is regulation (still). And yes, one regulation is the Truth in Lending Act. And yes, chargebacks.

Increased oversight

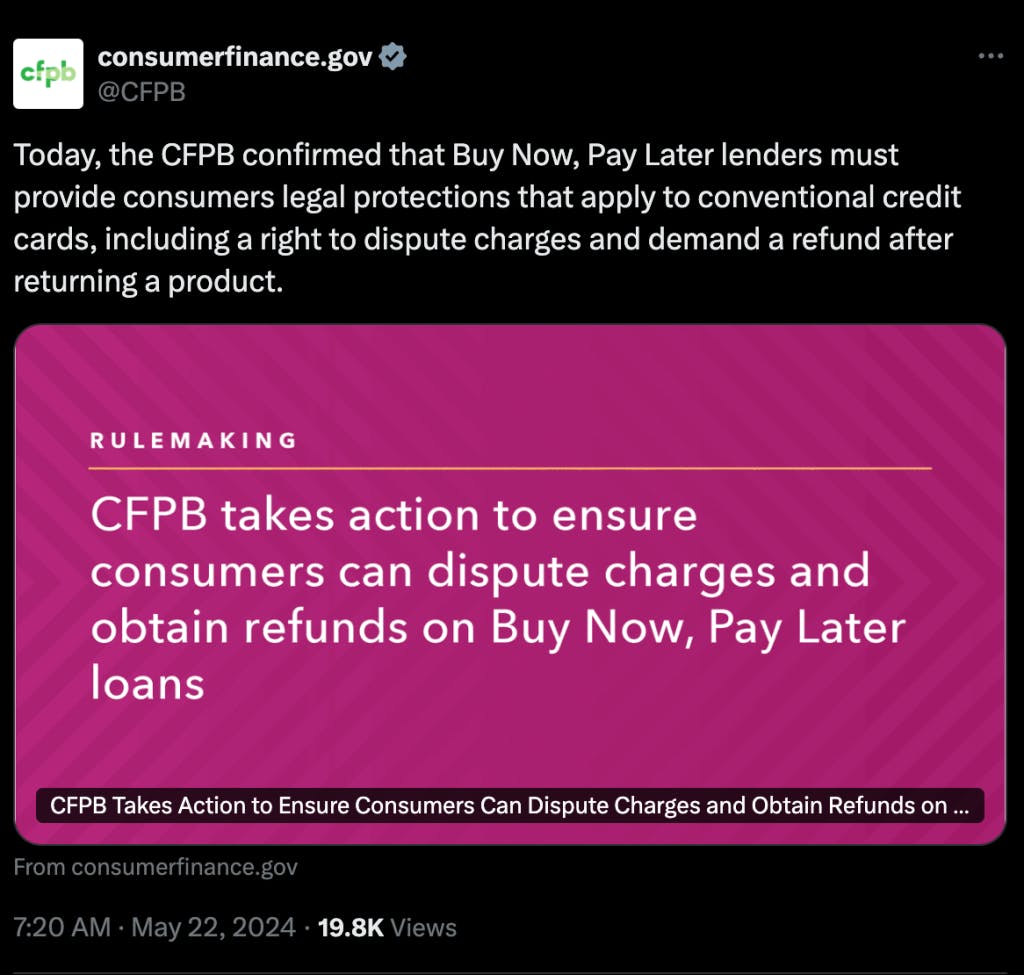

Starting in 2021, the US Consumer Finance Protection Bureau (CFPB) began studying BNPL apps. It released reports over the next couple of years that described consumer harms and high usage among the financially vulnerable.

In May 2024, the CFPB ruled that BNPL app users should have many of the same protections as credit card users:

Image from X.com.

As of July, pay-in-four loans now had to comply with relevant parts of TILA:

- Providing access to a dispute and refund process, including chargebacks.

- Providing statements to customers in a standard way to ensure they could manage their obligations, reducing overspending due to losing track.

Monthly loans were already subject to TILA, but the CFPB began taking a closer look at how the industry met any relevant consumer protection laws that were already on the books as well.

Which it did, in partnership with state regulators.

An industry group filed a lawsuit challenging the interpretive ruling in October, but that did not halt the examination, and the current status of the lawsuit is unclear.

The CFPB’s Supervisory Highlights for Q4 2024 included BNPL apps for the first time:

Examiners identified multiple violations of law including UDAAPs [unfair, deceptive, or abusive acts or practices] in connection with both Buy Now Pay Later and paycheck advance products.

Needless to say, you do not want to be a supervisory highlight, whether reported by a federal or state regulator.

One situation depicted in the report illustrates a way to become one: misrepresenting BNPL loan terms or costs.

Risk of misrepresenting loans

As discussed in the history section, inadequate or false disclosure of loan costs or terms is an example of a predatory lending practice.

Whether it’s on purpose or not, it’s brought to you by the letter D for deceptive.

The CFPB’s Supervisory Highlights report describes the relationship between merchants and BNPL providers as a partnership: merchants advertise loans on behalf of BNPL providers.

The report describes multiple situations where merchants advertised inaccurate BNPL loan costs or terms on their websites. The practice misled customers into signing up for loans with terms they didn’t want.

The experience of Consumer Reports policy analyst Chuck Bell illustrates how this may have happened.

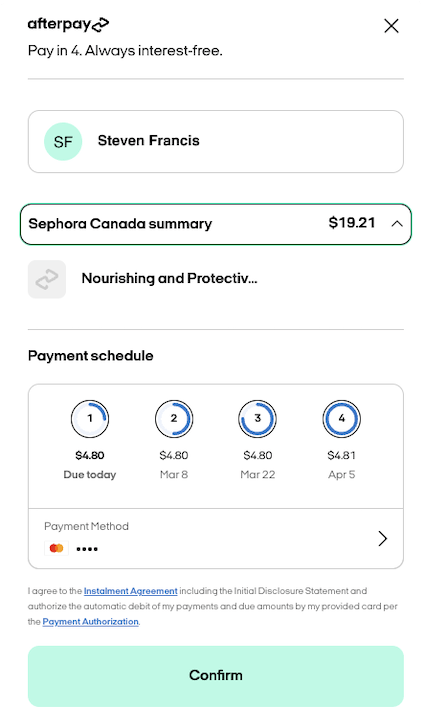

When buying high-value consumer electronics from an online retailer, Chuck was advertised a zero interest loan. He clicked on what he thought was that option, but the next screen was a list of loans over different terms—all with 15.99% interest.

Image from the CFPB.

Chuck was specifically looking for issues, but most people aren’t. That includes the customers referenced in the CFPB report. And as Chuck says:

It’s possible to click through pretty fast depending on the web checkout process.

It’s possible to click through pretty fast depending on the web checkout process.

In the CFPB case, the BNPL lenders were the ones breaking the law because the merchants were acting on their behalf. But the merchant partners suffered financial consequences as well (italics added):

In response to these findings, the lenders contacted the relevant merchants to ensure they updated their websites and refunded overcharges to customers. They also enhanced the marketing review process across merchant partners.

If Chuck had accidentally signed up for a 15.99% loan because of an experience implemented by the merchant, the merchant would owe him any interest and fees he had paid to the BNPL provider at that point.

Merchants then have to be extremely cautious about what information they share about loans, during checkout or otherwise, and that the flow matches the BNPL app.

As well as facing UDAAP issues related to more oversight, merchants selling to US buyers also lost a claimed advantage: that there were no chargebacks on BNPL transactions.

More chargebacks

When a US customer disputes a card charge, they do so through the chargeback process established under TILA. Similar consumer protections and processes exist in many countries outside the United States.

Chargeback processes offer important protections for consumers from fraud and poor-quality goods and services. But the experience for merchants managing them can be costly and time-consuming.

Chargebacks can also be a form of fraud against merchants: disputing a charge while keeping the good or service.

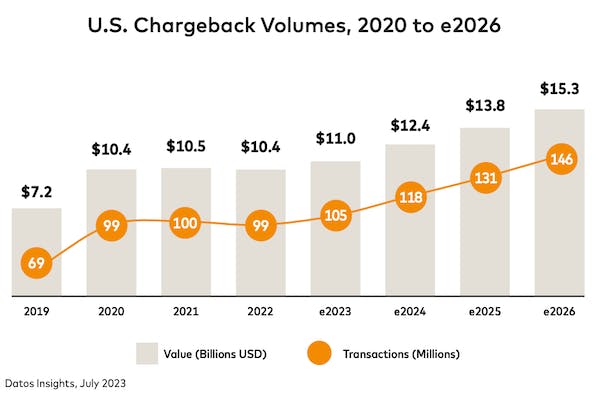

The number of chargebacks has only grown along with e-commerce sales as well. Mastercard published a thorough report on the current and projected state of chargebacks in the US and worldwide in 2023:

AP references how the CFPB ruling affected customers in a November 2024 article:

This holiday season, buy now, pay later users can also feel more confident if a transaction goes awry.

Which was good for US customers, but also meant that merchants faced increases in the number and complexity of disputes.

Buy Now, Pay Later providers may have a policy of shouldering the refund amount of chargebacks in cases of fraud, but the fraud section of this article outlines how that still costs merchants.

The future of financial product regulation in the United States is murky, but scrutiny of the industry is definitely not going away, and more can go awry than just transactions.

Global regulations

Regardless of what's happening in the United States, regulations on BNPL providers are increasing elsewhere in the world.

For example:

- BNPL services are already regulated as loans in Canada.

- Australia enacted regulation covering the industry in June 2024.

- The consultation period for the UK's regulatory approach ended in November 2024. Regulations are expected soon.

Uncertainty over regulations—let alone the regulations themselves—may further burden merchants.

Either could also contribute to service changes reducing the major merchant attractions to BNPL.

Service changes affecting key benefits

BNPL providers are mostly new companies, or new product lines in existing companies like PayPal. As a result, they are striving to scale rapidly or become profitable and stay that way.

For instance, business health can face increased financial scrutiny as well as regulatory scrutiny as companies prepare to IPO. Stock prices can also see dramatic shifts.

Because of business incentives like these, BNPL providers may make significant and rapid changes to their services.

As with a shifting regulatory environment, merchants are exposed to the danger that these changes may reduce key benefits like increased conversion and AOV.

A 2024 article published by the Federal Reserve Bank of Boston provides an example:

Most BNPL companies recently tightened their lending criteria in response to rising delinquencies.

A smaller pool of customers who are eligible for BNPL credit may limit expected increases in sales. (The optics of increasing sales to subprime customers will come up in the reputation section.)

It may also reduce viable partial payment options for merchants selling high-value products:

- Some customers may only be eligible for monthly loans at interest rates exceeding those of credit cards.

- Others may not be eligible for loans at all.

Of course, rising delinquencies didn't happen in a vacuum. Many borrowers using BNPL products are financially fragile to begin with and their experiences with BNPL may not be positive.

Negative customer encounters and negative press don't only affect BNPL providers, however. They can also reflect on merchants that implement BNPL apps.

Reputation risk

Offering payment by BNPL app can damage how people view your business in three related ways:

- Association with harmful business practices

- Entanglement with the provider during shared processes

- Increased risk of fraudulent transactions

Association with potential harms

Whether there are consumer risks to using BNPL apps or not is a settled question. There are.

The three major categories of potential harms to customers identified by the CFPB are:

- Inconsistent consumer protections: The kinds of safeguards that consumers expect from other finance products may not exist.

- Debt accumulation and overextension: BNPL encourages financially stretched customers to take on more debt. Obligations may also not be tracked centrally. This may lead customers to be offered even more credit from different sources, contributing to a debt trap.

- Data harvesting and monetization: BNPL providers often push customers into their proprietary apps. This allows them to collect personal data at a level of detail not captured by credit card companies.

Individual BNPL providers may not see what they are doing as harmful or predatory. But the fact that consumer harms are a topic of research, legislation, media discourse, and online discussion means you face two issues:

- Customers may see your business as complicit in harms by choosing to offer BNPL.

- Customers may experience difficulties themselves and associate them with your brand, even if you are not involved.

Rolling out ex-BNPL executive Jeremy Solomon one more time here, so he can reference the negative customer and merchant impact of predatory lending in purchase finance:

Incumbents profited most on borrower mistakes, making customers irate and negatively impacting the merchant’s brand and image.

Of course, there's another issue here too. Customers can also experience difficulties that you are involved in, along with the BNPL provider.

Shared business processes

BNPL providers maintain a connection with the customer after the order is placed. As a result, shared business processes can also be a risk to how customers see you.

Take the case of returns again. If the customer wants to return a pair of jeans, it's not as simple as contacting you.

The customer has the added wrinkle that they still owe the BNPL provider money.

Image from PxHere.

As Emily Stewart says in Vox, they could be "walking around in pants that aren’t technically paid off."

They have to follow both your policies and the BNPL provider's. Coordinating customer support between organizations is already difficult for everyone involved.

American Express explains customer expectations in this area:

Today’s customer expects a seamless experience no matter where or how they shop—and that includes returns.

Issues that are your store's responsibility and those that are not may bleed together.

As a result, American Express shares a warning for merchants:

You should also prepare for the fact that a customer who has a poor experience with the BNPL provider might inadvertently blame your business.

And, as alluded to before, if the customer does make a distinction, they may still knowingly blame you through association.

There is also another way that multiple parties may blame your business for a BNPL-specific risk: fraud.

Increased fraud risk

Stores that use BNPL apps are particularly vulnerable to fraudulent orders. This is because of three main factors, according to payment processor Checkout.com:

- Real-time decision-making: There is limited time to confirm the identity of the customer and that they intend to make the purchase.

- Delayed repayment: Paying over installments means there is a set period of time for someone to defraud and disappear.

- No credit checks: Often BNPL apps conduct "soft" risk analysis based on their own models rather than more extensive "hard" traditional credit checks.

That said, if there are unauthorized charges on a card holder's BNPL account, the provider does often accept liability. But the investigation is unlikely to be quick or painless for everyone involved.

Image by Mohamed Hasan from PxHere.

Furthermore, the BNPL provider won't reimburse you for any goods you shipped or services you provided.

Most importantly, there are reputation issues connected to BNPL fraud, as Checkout.com explains:

For merchants, the biggest risk if they fail to prevent BNPL fraud is reputational damage, which could impact relationships with customers, suppliers, and even BNPL providers.

Customers and suppliers may lose trust in your business. The provider may even terminate their relationship with you rather than face further losses.

On that note, this discussion is going to terminate here and move on to the takeaways.

Takeaways for merchants

The primary selling point of BNPL for merchants is a potential increase in revenue while still receiving payment up front.

BNPL apps accomplish this by turning hesitant customers into committed customers. As a merchant, you may then see higher conversion, lower abandoned carts, and higher AOV.

The line "he who hesitates is lost" may have evolved from an 18th century play by a man thinking about the Roman Empire.

But hesitating before committing can be a good thing, both for customers making a purchase—and for the e-commerce businesses serving them.

For each advantage for merchants of implementing BNPL, there are multiple overlapping dangers:

- Reduced margin may offset increased revenue. Merchant transaction fees can be very high, particularly on high-value goods. This also limits the advantage of getting the payment up front. Returns are higher on impulse purchases.

- Efficiencies connected to limited regulation may disappear. Globally, regulation of BNPL providers is increasing, leading to further obligations for merchants. The federal regulation situation in the US is uncertain, but merchants currently have the financial and operational burden of managing chargebacks on BNPL purchases in the US, and states also enforce revelant laws.

- Service changes may reduce primary benefits. BNPL providers have rapidly changing business needs and may make significant and rapid decisions reducing merchant advantages. For example, providers recently tightened lending criteria. This limits a major driver of increased conversion and AOV and reduces lending options available for high-value items.

- Reputation damage connected to BNPL providers may reduce conversion and impact relationships. Customers may associate your business with the consumer harms linked to BNPL providers. This can be in general, or because they have experienced them themselves. Customers may blame you for any issues with complex business processes shared with BNPL providers, like returns. Increased fraudulent orders can impact relationships with customers, suppliers, and BNPL providers, as well as costing time and money.

In other words, going back to Emily Thompson in Vox:

The thing about buy now, pay later is that the later part always comes.

Truer words, etc. But this piece isn't going to end on a down note.

At least, not a totally down note. A percentage-down-and-the-rest-later note.

Interested?

In the final section, learn about how Downpay fits into the e-commerce payment landscape and what business models it services.

Bringing back layaway with Downpay

Maybe your business sells high-value products with fulfillment delays through Shopify and you're struggling with abandoned cart problems discounts can't fix.

Maybe you offer:

- Bespoke jewelry like Cathy Shen's store Ma Folie

- Custom Amish furniture like retailer Modern Bungalow

- Pre-orders on new products like driving tech company OOONO

Or maybe customers want you to hold an item until their cash flow allows them to pay the whole cost. In other words, to offer a layaway plan, a.k.a., Buy Later, Pay Later.

If any of these sound like you, consider an embedded experience that:

- Doesn't involve loans, credit checks, or redirects

- Offers huge cost savings, especially on high value items

- Includes less risk

The Downpay Shopify app allows merchants to offer a deposit or layaway purchase option integrated into the Shopify checkout UI. Downpay was even built by a core team of Shopify alumni.

With Downpay enabled, your customers can choose to pay a deposit and store their payment information. You can then charge it later.

For custom-made goods and pre-orders you can then collect the rest when the order is ready to fulfill.

For a layaway plan, you can fulfill the order when you have collected the rest.

Either way, you and your customers can work out payment plans that meet both your needs. There's no intermediary with its own business interests.

And no concerns about truth in lending regulations—because it's not a loan.

Instead, Downpay operates under an established legal framework, merchant initiated transactions, that is much less likely to see changes.

The Grail Knight in Indiana Jones and the Last Crusade sums this whole adventure up well:

If you're looking for the Holy Grail of commerce, you must make a risk assessment, but assess the risks wisely. For while the true Grail may enable business success, the false Grail may take it from you.

Something like that, anyway.

11 proven strategies for improving conversion with deposits on Shopify

Learn how to share your store's deposit features with customers. Build trust and reduce friction with Downpay.

By signing up, you agree to receive marketing emails. View our privacy policy and terms of service for more info.