How deposits with Downpay saved Ma Folie 95% over Buy Now, Pay Later Shopify apps

Using Downpay for deposits on Shopify, Ma Folie offers a split payment plan that meets customer needs for a fraction of Buy Now Pay Later Shopify app fees.

Bespoke engagement rings and the madness of Buy Now, Pay Later transaction fees

By convention, an engagement ring has to have a diamond on it.

But Cathy Shen knows love doesn't follow convention, and her bespoke engagement ring company celebrates that.

Ma Folie specializes in rings featuring sapphires, emeralds, and rubies, as well as modern diamond rings, each as unique as the couple whose relationship they represent.

After Cathy launched her online store on Shopify, she learned that her customers wanted more flexibility in payment terms. At first she could only accept the whole payment up front.

Cathy first considered setting up a Buy Now, Pay Later (BNPL) app to provide a split payment option.

BNPL services offer customers a loan for the full price of their purchase during checkout. Customers pay off the loan in installments. Merchants pay the provider a fee per transaction.

But BNPL providers do not provide good value for merchants or customers on big-ticket items like made-to-order jewelry.

Spoiler: it has to do with the super high fees.

Cathy decided instead to set up a deposit purchase option using the Downpay Shopify app. Customers have overwhelmingly chosen to use it, and Cathy's business has seen enormous savings compared to BNPL apps.

Read on to learn about:

- The story behind Ma Folie

- The problem Cathy faced meeting customer payment needs

- Why BNPL Shopify apps didn't work for Ma Folie

- How Cathy set up Downpay for flexible payments on Shopify

- How using Downpay satisfied her customers and saved her money

The story: Cathy Shen's mad love

I became obsessed with sapphires.

— Cathy Shen, Ma Folie

Cathy Shen first had the idea to start Ma Folie after her now-husband Blair gave her a unique engagement ring. It had an oval pink sapphire set in rose gold and was like nothing she'd seen before.

Blair's proposal, which took place on a Ferris wheel in Siena, Italy, was an inflection point for Cathy in more ways than one.

"I became obsessed with sapphires and gemstones in general," Cathy says. (She was already obsessed with Blair, and vice versa.)

Here they are being obsessed with each other at their wedding.

Cathy's newfound fascination with precious stones set her on a path to a career change.

She would start a company that would make bespoke engagement rings as special to others as the one Blair gave her.

Cathy began taking courses from the Gemological Institute of America (GIA), achieving an Applied Jewelry Professional diploma.

Then she took a leap, quit her job, and launched her custom jewelry business.

Starting Ma Folie

Ma Folie means "my madness" in French. Cathy chose the name because an engagement ring symbolizes the "mad love" shared between individuals—and also because it reflects her passion for gemstones.

Cathy's company sells made-to-order engagement rings, crafted from scratch by skilled jewelers in Canada with gold bands that highlight natural sapphires, emeralds, and rubies. Ma Folie also offers natural or lab-grown diamonds.

No matter the gem, Ma Folie works only with recognized suppliers who source ethically produced gemstones.

Rings can be fully custom or based on one of several designs available in the online store. Ma Folie also has a collection of ready-to-ship rings.

This ready-made ring from Ma Folie, featuring a light green marquise Montana sapphire and a diamond, is also one of a kind.

For fully custom orders, Ma Folie has a thoughtful experience for customers:

- The customer books a consultation online or in person.

- At the consultation, they work with Cathy to explain what they want and then decide on the specifics of the design.

- Cathy sends them a quote and a link to a matching private product on Ma Folie's Shopify store.

- They complete checkout, committing to payment terms before Ma Folie begins production.

- Cathy involves the customer throughout production, including having them select the exact gemstones that will appear in the ring.

- After their final sign-off, the customer receives the ring.

Setting up this process required some polishing, however.

The challenge: Split payments on Shopify

That's when I just started searching for different apps.

— Cathy Shen, Ma Folie

Initially, customers had to pay the entire cost on checkout before Ma Folie would begin production on their ring.

"When I first launched, I thought people would just pay up front," Cathy says.

But customers shared that managing their funds to pay in advance could be tough. So, by a couple of months in, Cathy knew she needed a way to collect deferred payment.

She wanted to meet her customers in the middle:

- Make sure they committed to payment before Ma Folie began production.

- Relieve some of the financial pressure of making a significant purchase.

Cathy saw that other jewelers offered partial payment plans.

"I didn't know how they did it," she says. "But that's when I just started searching for different apps."

She began her research with Buy Now, Pay Later apps.

Not the solution: Buy Now, Pay Later

I’m not paying 8 to 10%. That’s ridiculous.

— Cathy Shen, Ma Folie

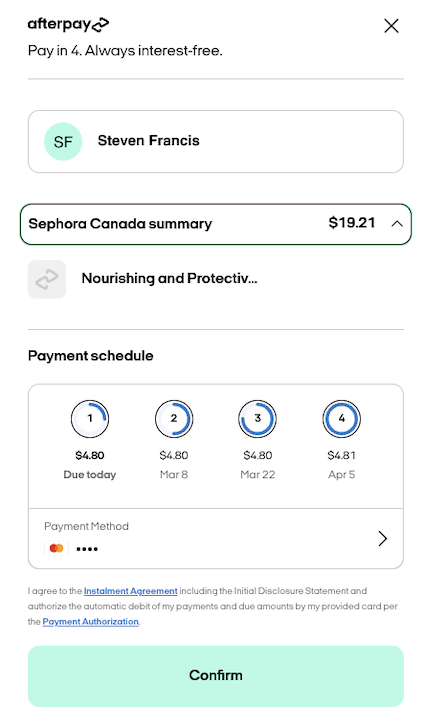

Buy Now, Pay Later services that integrate with Shopify like Affirm, Klarna, and Afterpay offer loans as a payment method on checkout.

Confirming a BNPL loan for a purchase using Afterpay.

In Cathy's case, the BNPL provider would cover the full price of the ring, and the customer would pay off the loan on a schedule.

Cathy would owe the provider a fee calculated as a percentage of each order transaction.

This percentage is higher for high-value orders like engagement rings, since the provider takes on more risk.

Deciding against Buy Now, Pay Later

The deciding factor for Cathy was these merchant transaction fees: using a Buy Now, Pay Later app would take an unworkable percentage of her sales in exchange for limited benefit.

"My products are very high value already," Cathy says. "So for them to take 8% or 10%, it was just too much for my business to handle."

For example, if a merchant sold $15,000 in a month, at that rate, they would be charged $1500:

$10% * $15,000.00 = $1500.00

Plus, the main advantage BNPL apps have for merchants didn't apply to Cathy's selling strategy.

Because the provider takes on the risk, merchants can be comfortable shipping an in-stock item right away.

With preorders and made-to-order products—like Cathy's engagement rings—the product doesn't exist at first. The merchant also doesn't ship until payment is completed.

Cathy therefore didn't need the same level of risk covered. BNPL services then offered little to Cathy in exchange for the sky-high fees.

"So I'm not paying 8 to 10%," she says. "That's ridiculous."

Madness, even.

But now Cathy had another approach in mind. There was a time-honored method for securing big-ticket items that aren't yet available: deposits.

The solution: Deposits with Downpay

I like the deposit method because it guarantees me that they're in. And it gives comfort to the client.

— Cathy Shen, Ma Folie

From pre-ordering a product that isn't out yet, to booking an appointment, customers are used to splitting large payments into two:

- A deposit in advance

- The rest when they receive the item or service

Deposits are also common for made-to-order goods with long lead times. These include custom furniture, portraits, and, of course, jewelry.

"I like the deposit method because it guarantees me that they're in," Cathy says. "They've committed to the product. And it gives comfort to the client to say, 'your ring is not done, but we're working on it and you can split your payment up into two.'"

Looking for a way to set up this payment experience, Cathy soon found the Downpay app.

Enter Downpay

Downpay, built by a core team of Shopify alumni, lets merchants offer a deposit purchase option.

Customers can choose to pay a set percentage on checkout and store their payment information. Then the merchant can collect the remainder when the order is ready.

Downpay charges merchants a monthly subscription fee, with tiers based on the number of Downpay-processed orders.

Cathy did the math, and for her expected order volume, the pricing was exponentially better than paying a 10% BNPL transaction fee on each purchase. (She'd see just how much better once she started processing sales through Downpay.)

Deciding on Downpay

Cathy was able to set the app up herself to try it out.

"I'm not a techie person," Cathy says. "But I did my best and installed it with the instructions. It's super easy."

Making a decision was straightforward. The deferred payment app did exactly what she wanted at a price that made sense for her business.

"I can split the payment into two," she says. "One before I make the ring and the final payment right before the ring is ready to be shipped out."

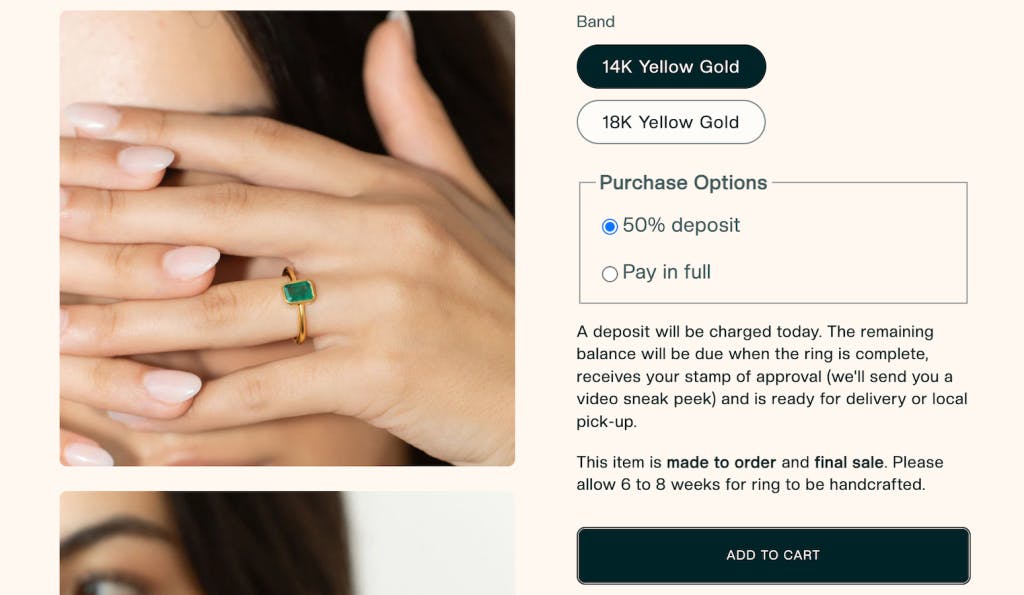

Made-to-order engagement ring product page with up front and 50% deposit purchase options.

(You can explore more of how Downpay works yourself in the interactive demo.)

After Downpay support walked her through some more adjustments to fit her business, Cathy was more than satisfied.

She was ready to give her customers the payment flexibility they wanted, so that they could more easily have their dream engagement rings made real.

The results: Total customer takeup and huge savings

For my made-to-order rings, 100% of my customers use the deposit method through Downpay.

— Cathy Shen, Ma Folie

Cathy has now been using Downpay to offer her customers a 50% deposit option for over a year.

They have taken full advantage of it, and Cathy's business has saved an immense amount of money over using a Buy Now, Pay Later app.

Made-to-order

customers using

deposits

Monthly savings

over BNPL

apps

What customers think

Customers for Ma Folie's bespoke rings have provided great feedback on the deposit purchase option. "Everyone's been very happy about that option," Cathy says.

In fact, they are so happy that they all use it instead of choosing to pay up front.

"For my made-to-order rings, 100% of my customers use the deposit method through Downpay," Cathy continues. "I haven't had a single person pay up front."

Her customers also highlighted a benefit compared to Buy Now, Pay Later apps: "People also prefer the longer lead time between credit card payments."

BNPL loans usually require payments biweekly or monthly. This frequency doesn't make sense for the customers of a made-to-order business. Nobody wants to pay off the full cost of something that doesn't exist yet on a biweekly schedule with the added risk of late fees.

The deposit payment option Cathy set up with Downpay instead allows customers to manage their own funds while Ma Folie handcrafts their rings.

And money changes hands when it meets both customer needs and Cathy's, not the revenue model of a BNPL provider.

Merchant savings

When it comes to Cathy's own financial planning, using Downpay meant she paid only 5% of the monthly cost she would have paid if she had set up a Buy Now, Pay Later app instead.

"If I had used a Buy Now, Pay Later method, it would have cost me twenty times as much," Cathy says. "The savings right there are enough to go with Downpay."

With the deferred payments piece of the puzzle in place, now Cathy can focus again on her first (well, second) love—gems.

Further reading

Check out other case studies to learn how Downpay enables more sales for Shopify merchants.